South Asia’s energy crisis is no longer just about blackouts and angry households. It has become a test of whether the region’s growth model can survive repeated external shocks. When oil and LNG prices jump, the pain does not stop at ports or power plants. It spreads into factory schedules, fertilizer output, export margins, fiscal balances, and inflation. In rich countries, that sort of shock is expensive. In poorer and underdeveloping economies, it can become destabilising.

That risk has sharpened again in late March 2026. Reuters reported on March 27 that Brent crude had risen more than 50% since the Iran war began, briefly topping $119 a barrel, and that analysts surveyed by Reuters saw average prices around $134.62 under current disruption scenarios. A day earlier, Reuters reported that Asian LNG prices had surged 143% since late February and were now far above the rough $10 per mmBtu level at which demand from emerging Asian buyers is more sustainable. For South Asia, where energy import dependence remains high and power systems are often financially weak, that is not just a commodities story. It is a growth story.

The economic outlook was already looking pretty grim. The World Bank laid out a pretty gloomy picture in its October 2025 South Asia Development Update, forecasting that the region is going to see a sharp decline in growth – from 6.6% in 2025 to 5.8% in 2026. And things are only set to get worse: the Bank warned that South Asia is sitting pretty vulnerable to economic shocks and that the weakness of the electricity systems is only making it easier for the region to be hit by global energy price increases. The Bank’s follow-up update in January 2026 said that South Asia actually managed to grow at 7.1% in 2025 because of India’s remarkable resilience – but it still drives home the fact that the region is basically on edge, just waiting for the next big stress test.

It’s pretty clear that growth is patchy across the region but the underlying issues are all pretty much the same. Bangladesh is just one example of this – it’s on the verge of turning a energy crisis into a full-blown export crisis because its economy is so dependent on the garment trade. In Pakistan, they’ve got a bit of a safety net against the immediate LNG price pressure, but its power sector is still crippled by a mountain of debt – and that’s a structural problem that’s not going to be fixed overnight. India is doing a bit better, but even it’s only holding on because it’s got a solid supply of coal, emergency measures in place and is trying to get its renewable energy act together. Sri Lanka’s had a pretty good recovery from the disaster of 2022, but it’s still living hand to mouth on imported fuel, is only just starting to rebuild confidence and is relying on emergency supplies whenever the markets turn against it.

What South Asia’s leaders still get wrong about the energy crisis

The most dangerous mistake in South Asia is no longer the fuel shortage itself. It is the habit of treating each new energy shock as a temporary emergency rather than as evidence of a structural weakness. Governments still respond as if the crisis will pass and the old growth model will resume: subsidise a little more, ration a little longer, borrow a little extra, and wait for global prices to ease. That approach may prevent immediate collapse, but it does not build resilience.

The region’s underlying problem is now plain. Too many governments still want industrial growth, export competitiveness, and urban expansion without first building energy systems strong enough to support them. Cheap labour, ambitious factories, and rising demand can take an economy only so far. When power remains unreliable and imported fuel remains central, growth becomes less durable than it appears. South Asia’s energy weakness is no longer a side issue in development. It is one of the main reasons development keeps becoming more fragile under pressure.

Why energy stress hits developing economies harder

Developing economies suffer energy shocks differently because they have less room to absorb them. Governments can let tariffs rise and accept inflation, subsidise more and damage public finances, or ration and shift the cost into lower output. South Asia has spent years moving among those three choices. The World Bank has warned that the region’s vulnerability is amplified by significant electricity transmission losses and frequent power outages, and that more decentralised renewable generation and grid modernisation would improve reliability and energy security.

The current shock also arrives at a moment when policymakers have less flexibility than before. Pakistan remains under IMF discipline. Sri Lanka is still navigating IMF-linked recovery. Bangladesh is seeking additional external financing to manage fuel and LNG imports. Even India, the strongest system in this group, is leaning on coal, solar, and battery storage in a coordinated stress response rather than behaving as if the market shock were minor.

When power fails, growth slows

Power shortages look like a utility problem from the outside, but firms experience them as a planning problem. Production lines slow, backup generation gets costly, delivery schedules slip, and working capital tightens. Industries that compete internationally do not lose only when the lights go out. They lose when energy becomes too volatile to price into contracts or too expensive to smooth over with generators. Reuters reported on March 26 that price-sensitive countries such as Bangladesh, India, and Pakistan were already showing demand destruction and switching away from LNG as prices rose.

That matters because South Asia’s growth model is more energy-intensive than it often appears. Industrialisation, export manufacturing, transport, cold chains, fertilizer production, and urban services all depend on stable power. The World Bank noted that India’s annual peak power demand and electricity demand have been growing by 5% and 6%, respectively, and that installed generation capacity reached 500 GW in September 2025. That is the profile of a region still building growth on rising energy use, not one that can glide through a fuel shock unscathed.

Bangladesh’s garment economy and the cost of energy uncertainty

Why reliable power matters to Bangladesh’s export machine

Bangladesh is especially exposed because one sector matters so much. A World Bank blog in late 2025 said ready-made garments accounted for about 82% of the country’s exports. That concentration helped Bangladesh turn low-cost manufacturing into a development engine. It also means that an energy problem quickly becomes an export problem.

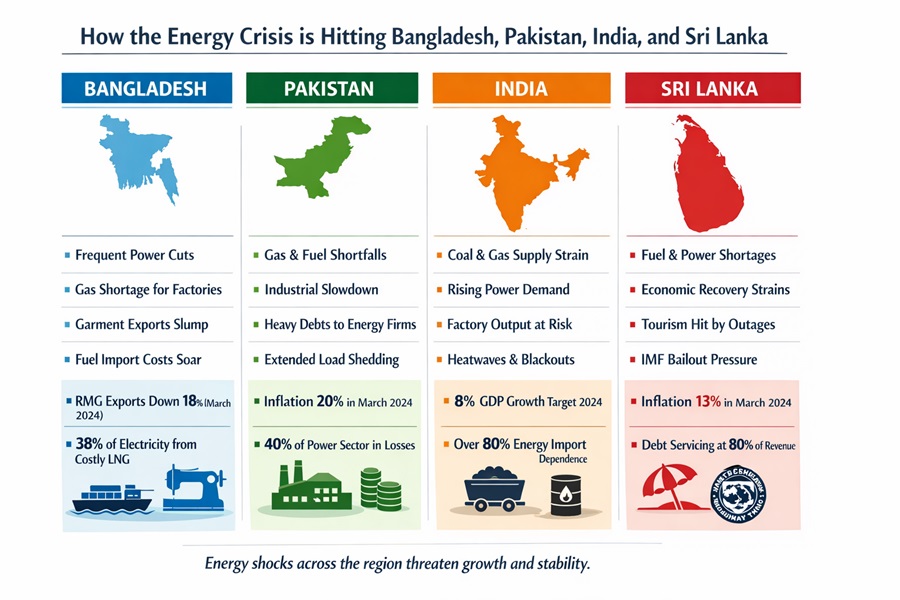

Reuters reported on March 10 that Bangladesh, with a population of about 175m, imports roughly 95% of its energy needs. During the current fuel squeeze, the government imposed fuel rationing, restricted diesel sales, and closed universities, while garment manufacturers said power cuts had doubled to as much as five hours a day since the war began on February 28. For a garment exporter, five hours is not a minor inconvenience. It is lost machine time in an industry built on deadlines, tight margins, and buyer expectations that do not soften because the grid does.

Gas shortages, rising costs, and margin pressure in garment manufacturing

Bangladesh’s problem is not only electricity. It is the combination of weak grid supply, diesel scarcity, and gas diversion. Reuters reported that the country normally needs about 380,000 metric tons of diesel a month, but rationing had pushed one estimate of demand down to roughly 270,000 tons. That reduction does not signal improved efficiency. It signals suppressed activity. Less diesel means less transport, less backup generation, and less flexibility for industry to compensate for public power failures.

The gas side is just as serious. Reuters said severe shortages had forced four of Bangladesh’s five state-owned fertilizer plants to halt operations so gas could be redirected to power generation. That is a revealing sign of stress. It shows the state moving molecules from one productive use to another simply to keep the wider system running. Economies under energy pressure often do not solve shortages; they reallocate them.

Dhaka’s financing response shows how narrow the room for manoeuvre has become. Reuters reported on March 20 that Bangladesh was seeking more than $2bn in external financing from lenders including the IMF, World Bank, ADB, AIIB, and ITFC to mitigate its fuel and LNG crisis. That is a rational emergency move, but it also underlines the point: Bangladesh is not merely paying higher energy prices. It is borrowing to keep paying them.

What energy stress means for jobs and export resilience

The longer-term risk is competitive erosion. Bangladesh’s garment sector has succeeded by combining scale, labour availability, and buyer trust. Energy instability weakens all three. Orders become harder to schedule, production costs rise through generator fuel or idle capacity, and smaller suppliers become more vulnerable than large export groups with more financial cushioning. When a country’s main export sector must keep explaining late deliveries through fuel and power shortages, it is not just having an energy problem. It is quietly losing part of the development bargain that made industrial growth possible in the first place.

Pakistan’s industrial strain and the burden of a fragile power sector

Why Pakistan’s energy problem is also an industrial-policy problem

Pakistan’s situation is more complicated than Bangladesh’s because the immediate LNG shock and the structural power-sector problem are not the same thing. Reuters reported on March 13 that Pakistan’s power minister said 74% of the country’s electricity now comes from local sources and that LNG accounts for about 10% of power generation. The government’s aim is to raise the local share above 96% by 2034. That gives Islamabad a plausible short-term argument: the country is not as exposed to imported gas for power as it once was.

But that is only part of the picture. Pakistan’s industrial problem is not just fuel dependence. It is the accumulated weakness of a power system that has struggled for years with recoveries, losses, tariff politics, and debt. The IMF’s May 2025 report on Pakistan said circular debt in the power sector had continued to accumulate into February 2025 and made clear that cost-reducing reforms were the only sustainable route to viability and lower tariffs. That matters because industry does not judge the system by fuel mix alone. It judges it by whether power is reliable, payable, and predictable.

High power costs, low confidence, and slower factory activity

Even where supply is available, cost remains a brake. Reuters reported in February that Pakistan was discussing electricity-tariff revisions with the IMF and that analysts expected the overhaul to push up inflation while easing some pressure on industry. That tension is central to the country’s manufacturing dilemma. If tariffs stay too high, industry loses competitiveness. If tariffs are cut without fixing the underlying financial mess, the problem simply reappears elsewhere in the system.

The recent LNG shock is already spilling into the real economy. Reuters reported on March 26 that Pakistan was among the countries experiencing demand destruction as prices rose, with rationing through a four-day work week and weaker activity in sectors such as fertilizers and textiles. “Demand destruction” can sound abstract. In practice it means factories reducing production because the economics no longer work. That is not adjustment in a healthy sense. It is contraction disguised as conservation.

How energy stress feeds broader economic fragility

Pakistan has made some progress in restoring macroeconomic stability. Reuters reported today that Pakistan and the IMF had reached a staff-level agreement on a $1.2bn disbursement, which would take total disbursements under the current program to $4.5bn, pending board approval. Reuters also noted that Pakistan’s central bank kept its benchmark interest rate at 10.5% this month, citing global energy prices and regional tensions as inflation risks for an import-reliant economy. Those are stabilising moves, but they do not remove the structural weakness. They mostly buy time against it.

Pakistan therefore faces two energy truths at once. The first is that greater reliance on domestic power sources gives it some short-term insulation. The second is that a system weighed down by circular debt and tariff distortions still struggles to support durable industrial growth. Energy shocks in such a system do not need to be catastrophic to be harmful. They need only be frequent enough to keep confidence low.

India’s manufacturing ambitions depend on keeping power reliable and affordable

Manufacturing growth needs more than new factories

India is stronger than its neighbours in this story, but not untouched. The World Bank estimated in January 2026 that India’s economy would grow by 7.2% in FY2025/26, helping keep South Asia’s overall growth rate elevated. That scale matters. It gives India more policy and fuel options than Bangladesh, Pakistan, or Sri Lanka. Yet a fast-growing manufacturing economy needs more than new plants and industrial parks. It needs the boring thing that makes everything else work: stable electricity at scale.

India’s balancing act between coal, renewables, and demand surges

Reuters reported on March 21 that gas accounts for only around 2% of India’s total power generation, though about 8 GW is used during peak demand or heatwaves. The government said it expected solar generation to help meet daytime demand of up to 270 GW, was speeding up battery storage, and anticipated a 4 GW coal plant in Gujarat returning to service. Reuters also reported that India had produced 1bn metric tons of coal for the second straight year and had around 210m metric tons of coal stock, enough for about 88 days of consumption, with coal still supplying roughly three-quarters of electricity.

That combination explains India’s relative resilience. It is not relying on one answer. It is using coal as the backbone, renewables as daytime relief, batteries as evening support, and administrative coordination to keep the system from tightening too far. This is a more robust posture than that of its neighbours. It is also an admission that the system is being actively stress-managed. Resilience here means having enough levers to pull, not being free of risk.

Can India protect industrial growth from the next energy shock?

India’s challenge is more strategic than existential. Reuters reported on March 26 that the wider LNG shock was already hitting petrochemical and ceramic production. So the risk is less about mass rationing and more about cost pressure in specific industries, especially when peak demand is climbing and heatwaves make balancing harder. India can keep the lights on more easily than its neighbours, but doing so may require heavier coal use, faster storage deployment, and continued fuel diplomacy, including fresh attention to Russian supplies, according to Reuters reporting from March 27.

That is the important distinction. India has buffers. But those buffers come with trade-offs in fuel mix, emissions, and procurement strategy. The country is not escaping the regional energy story. It is managing it better than the rest.

Sri Lanka’s recovery still depends on energy stability

The energy lessons of Sri Lanka’s economic collapse

Sri Lanka remains the most psychologically exposed country in this group because it has recent memory of what a full energy-and-foreign-exchange breakdown looks like. The World Bank said in April 2025 that Sri Lanka’s economy grew 5% in 2024, driven by a rebound in industry and tourism-related services. It also noted that the country’s recovery had outpaced projections, even as poverty reduction and medium-term resilience still required more work. That recovery is real. It is also fragile.

Why recovery is fragile without stable power and fuel supply

Reuters reported on March 17 that Sri Lanka had approved emergency spot purchases to cover a fuel shortfall of more than 90,000 metric tons, launched new tenders for petrol, diesel, and crude, and approved emergency procurement of 300,000 tons of coal from India to avoid power disruptions. It also reported that the government had declared Wednesdays a holiday for public officials and launched fuel rationing, while directing extra supplies toward agriculture, fishing, and tourism. Those are emergency-management tools, not the normal operating pattern of a comfortably recovered economy.

A week later, Reuters reported that Sri Lanka’s central bank held its policy rate at 7.75%, citing global uncertainty from the Middle East conflict. Reuters said the central bank viewed reserves of $7.3bn as a buffer and still expected 4-5% growth in 2026, but also noted that fuel prices had risen about 35% this month and that prolonged conflict could weigh on domestic activity. That combination captures Sri Lanka’s present condition almost perfectly: improved, but not secure.

Has Sri Lanka reduced its energy vulnerability enough?

Not yet. Sri Lanka’s macro numbers have improved, but it still depends heavily on imported fuel and on public confidence that shortages and queues will not return. Emergency spot buying, rationing, and weekly shutdown measures all carry a practical cost, but they also carry a political memory. Recovery depends not just on reserve levels or IMF reviews. It depends on ordinary citizens believing that the state can keep basic systems working without slipping back into improvised crisis management. Every visible fuel-control measure makes that belief a little harder to sustain.

The hidden cost of the energy crisis: inflation, jobs, and household pressure

Why energy inflation reaches far beyond the utility bill

Energy inflation is never confined to energy. Oil affects transport, food prices, freight, fertilizer, and commuting costs. LNG shortages push countries back toward coal or rationing, which has knock-on effects on industry and public services. Reuters reported on March 27 that South and Southeast Asia were among the regions likely to face fuel shortages and rationing under prolonged disruption scenarios. A day earlier, Reuters cited ADB analysis suggesting that if Middle East energy disruptions persisted for more than a year, inflation in developing Asia and the Pacific could rise by as much as 3.2 percentage points and growth could fall by up to 1.3 percentage points over 2026-27.

Factory stress becomes worker stress

The industrial pain eventually lands on workers. When factories cut machine hours, reduce output, or run fewer shifts, workers lose overtime, informal earnings, or jobs altogether. Bangladesh’s garment sector, Pakistan’s textiles and fertilizers, India’s energy-intensive manufacturing pockets, and Sri Lanka’s tourism-linked transport economy all feel the same squeeze in different forms. Energy stress starts with systems and balance sheets, but it reaches households through lower hours, higher prices, and more fragile employment.

The unequal burden on low-income households

Poorer households suffer more because they have fewer ways to smooth the shock. They spend more of their income on transport, food, and energy-adjacent essentials, and they are less able to absorb lost working hours or tariff increases. Governments know this, which is why they often reach first for subsidies or controlled prices. Yet those protections are fiscally hard to sustain when countries are also financing imports externally or operating under IMF programs. South Asia’s recurring energy dilemma is therefore also a distributional one: who absorbs the shock when the state cannot fully do so anymore?

Why South Asia cannot build a strong growth story on weak energy systems

Export competitiveness now depends on energy security

For years, much of South Asia’s development story rested on labour cost, urbanisation, and market size. Those advantages still matter. But they do not compensate indefinitely for expensive or unreliable power. Export industries compete on delivery certainty as much as on wage levels. If outages, fuel rationing, or emergency procurement become routine, then energy insecurity starts eroding the very competitiveness these economies are trying to sell to investors and buyers.

Fiscal weakness and energy weakness reinforce each other

Weak energy systems are not only a technical problem. They are a fiscal one. Pakistan’s circular debt, Bangladesh’s search for multilateral financing to buy fuel, and Sri Lanka’s reliance on emergency procurement all show the same pattern: when the energy system weakens, the public balance sheet is pulled into the crisis. That in turn reduces room for growth-supporting spending elsewhere and makes future shocks more damaging.

A region of billions cannot afford chronic energy insecurity

This is the larger point. South Asia is home to some of the world’s biggest concentrations of workers, industrial ambition, and unmet development needs. Chronic energy insecurity therefore does not merely cause inconvenience. It slows structural transformation at massive scale. The World Bank has already warned that decentralised renewables, grid modernisation, and fewer import barriers on intermediates such as solar panels would improve energy security and reliability. The fact that such reforms remain urgent in 2026 tells its own story about the region’s unfinished development agenda.

The uncomfortable truth: South Asia is trying to grow on unstable power foundations

The region’s real problem is not simply that oil is expensive or LNG is volatile. It is that South Asia is still trying to build twenty-first century growth on energy foundations that remain too weak, too politicised, and too exposed to outside shocks. Bangladesh shows what happens when an export machine depends on power it cannot fully secure. Pakistan shows how a country can reduce one form of dependence while remaining trapped by a broken power economy. Sri Lanka shows how quickly a recovery loses credibility when energy stability remains uncertain. India, despite its greater depth, shows that even the strongest system in the region now needs constant balancing to stay ahead of demand and disruption.

That should worry policymakers more than the latest price spike. A temporary market shock can pass. A development model built on fragile energy systems will keep failing in slow motion. South Asia’s leaders often speak as though the next phase of growth will come from manufacturing, urbanisation, and rising domestic demand. It will not, at least not reliably, unless energy security is treated as core economic strategy rather than as a utility-sector problem. The next divide in South Asia may not be between reformers and laggards, or even between rich and poor states. It may be between countries that build resilient power systems in time and those that continue managing crisis after crisis.

What happens next if the region fails to adapt

If oil and LNG prices stay elevated, South Asia is likely to split into tiers. India will cope better by leaning on coal, solar, and storage. Bangladesh will keep paying up for fuel and LNG while trying to prevent its export engine from losing momentum. Pakistan will continue to combine partial fuel insulation with structural power-sector weakness. Sri Lanka will manage carefully, but every new price jump will test the political durability of recovery. Reuters reported that analysts expect LNG prices to remain elevated through at least 2027, which means this may not be a one-quarter disruption. It may be the beginning of a harder operating environment for the region’s import-dependent economies.

That is why the region’s energy story now belongs at the centre of its growth story. Bangladesh shows how quickly an export-led economy can run into a power-and-fuel wall. Pakistan shows that partial energy cushioning does not solve a structurally broken power balance sheet. India shows that size and coal bring resilience, but not immunity. Sri Lanka shows that recovery without secure fuel supply remains recovery on probation. South Asia’s underdeveloped and lower-income economies do not experience energy shocks as temporary discomfort. They experience them as a direct threat to industrialisation, macro stability, and daily life for vast populations.